Big data is playing a prominent role in life insurance this year.

Interest in coverage has surged during the pandemic, but for many people, social distancing mandates took the life insurance medical exam off the table. As consumers look for quick, noninvasive ways to buy policies, insurers have turned to accelerated underwriting, a process that uses big data and algorithms instead of exams to evaluate applicants.

While accelerated underwriting isn’t new, more than a third of life insurers have expanded it due to the pandemic, according to a study by the Society of Actuaries. And no-exam life insurance appeals to many people. “They want it to be fast and easy,” says Gina Birchall, chief operating officer for the life insurance trade group LIMRA.

How accelerated underwriting works

Companies typically use accelerated underwriting to fast-track healthy people’s applications. But now, they are offering it to consumers who are social distancing. Low-risk applicants are approved based on big data, while requiring medical exams for everyone else.

One big perk is that you still get fast-tracking. It takes around nine days for an insurer to reach a final decision using accelerated underwriting instead of the traditional 27+, according to LIMRA.

How much do you want to pay?

For people in less than perfect health, a policy with full medical underwriting is likely to be the cheapest option. But if you are in good health and wish to stay that way by avoiding the Covid-19 risk of exams, most insurers will offer contactless, accelerated underwriting to fast-track your application. Your price and product will likely be the same as if you had taken the exam.

You can get instant, term life quotes from dozens of A-rated life insurance carriers who offer accelerated underwriting at QualityTermLife.com.

Consumers think it’s too expensive and too complicated to buy – but it actually isn’t.

Young family at a prime age for inexpensive life insurance coverage.

The percentage of Americans who have a life insurance policy is declining, according to a new study by J.D. Power. Its 2020 U.S. Life Insurance New Business Study found that the decline is largely driven by consumers under the age of 45, many of whom consider life insurance unnecessary, too expensive, or too complicated to purchase.1

KEY TAKEAWAYS

The percentage of Americans with a life insurance policy is declining, according to a new J.D. Power study.

The decline is largely driven by people under age 45.

Many consumers consider life insurance unnecessary, too expensive, or too complicated.

Life Insurance Remains a Mystery to Many

Depending on the type of policy, life insurance can be expensive and complicated, as study respondents said. However, term insurance, which is generally the best option for most consumers, is cheap and relatively simple.

Unfortunately, the study found that the workings and benefits of life insurance policies still remain mysterious to consumers, which decreases the chances of them buying one. That can leave individuals and families financially devastated if a loved one passes away.

Life insurance professionals, including agents, advisors, and carriers, can help dispel some of the myths of life insurance and highlight the benefits, according to the study.

Specifically, J.D. Power recommends that insurance professionals make sure that prospects understand coverages and costs, and keep them up to date on the status of their application for insurance once it’s been submitted.

Other Findings of the J.D. Power Study

Among the study’s other findings:

Just 44% of consumers shop around and compare life insurance quotes from multiple insurers.

Roughly three-fourths of consumers who purchased a policy said they picked it because it had the lowest price.

Life insurance is a critical financial tool. Amazing that a primary reason consumers say they don’t purchase more life insurance is because it’s too expensive! It is one of the most reasonable and worthwhile investments you can make.

The obvious solution to this misconception is to make life check out actual rates. In fact, many websites provide life insurance rate comparisons online.

You can find instant, term life quotes from dozens of A-rated life insurance carriers at QualityTermLife.com.

Check it out now to see for yourself how inexpensive life insurance can be.

As the COVID-19 pandemic has spread, we’ve been reminded that illness and death can come at any time, and that has some people thinking seriously about life insurance.

If you’re wondering if you have enough life insurance, you may be asking yourself if you can even get life insurance during the pandemic. Read on for the answer to that question and more.

I’m not sick, but could COVID-19 affect whether I can get life insurance?

While neither the application process nor the underwriting criteria has changed substantially during the pandemic, some companies have added another step, asking applicants if have COVID-19.

With many agents offices closed, can I just apply online?

Yes. You can start the process online. QualityTermLife offers online quotes from dozens of A-rated insurance companies. You can always call to have a conversation about your options, budget and coverage.” Once you are submitted, all paperwork is completed online and on the phone with the insurance company.

But will I have to get a physical exam?

In many cases, no. Most insurance companies set a coverage amount – anywhere from $100,000 to $500,000 – that can be applied for without a physical exam. Most insurers have a streamlined underwriting process. If you are younger than age 50 and in reasonably good health, you may only have to do a phone interview to answer questions about your medical history.”

However, if something comes up in your interview that requires closer inspection, the company could require a simple medical exam that can either be completed in your home or in a testing facility. Of course, they are taking every precaution to make sure people won’t be exposed to the virus (COVID-19).

Young families are generally not buying life insurance, new data indicates.

Courtesy of LIMRA

Valentine’s Day brings thoughts of roses and chocolate, but have your clients thought about giving peace of mind? According to LIMRA research, 9 in 10 life insurance owners say that is what they get from purchasing life insurance.

LIMRA is joining Life Happens with its “Insure Your Love” campaign, which highlights the importance of protecting the ones you love through the purchase of life insurance.

More than half of American adults (57%) own some type of life insurance. Three in 10 consumers have life insurance coverage at work, while 4 in 10 have individual insurance.

The majority of Americans believe that most people need life insurance, and identify several reasons for owning it such as paying for final expenses (91%), replacing lost wages (66%), and leaving an inheritance (63%).

So, what prevents consumers from owning life insurance (or purchasing more)? The top three reasons: it is too expensive (63%), they have other financial priorities (61%), or they already have enough coverage (52%).

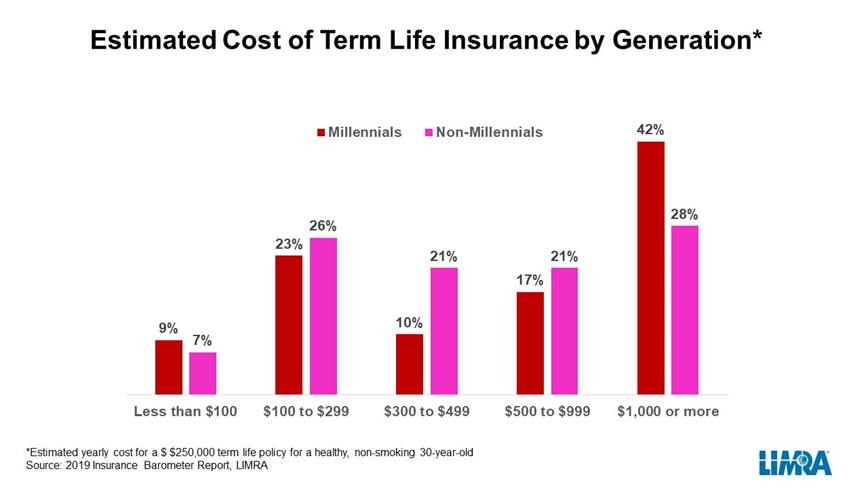

When it comes to cost, consumers generally overestimate the cost of owning life insurance. The Millennial generation, much more than Baby Boomers or Gen X, is likely to overestimate the price tag for term insurance.

In fact, in a recent LIMRA survey, only about a 1 in 4 consumers have a good idea of what a $250,000 term life policy would cost for a healthy, non-smoking 30-year-old (see chart). The actual cost for the policy is roughly $160 per year.

Life insurance is one of those things many of us don’t like to think about. Instead of looking into all the ways that life insurance could benefit us, we buy into the myths and misconceptions that tell us life insurance is too expensive, too complicated, or simply unnecessary.

The truth is, life insurance is none of those things — but it is really important. If you’ve been avoiding life insurance because of these myths, it’s time to learn the truth.

Top 5 Life Insurance Myths

Life insurance is expensive

Are you convinced you can’t afford life insurance? If you think life insurance costs are comparable to health or car insurance rates, you’re in for a pleasant surprise: If you’re a healthy non-smoker in your 30s, you could pay as little as $222 a year for $500,000 in coverage. That’s about $19 a month, or roughly the cost of a restaurant meal.

I can’t get life insurance because of a pre-existing condition

Many people pass on life insurance because they think that their pre-existing medical condition makes them too unhealthy to be accepted by insurers. The truth is that medical progress and the availability of preventative programs now allow many people with chronic conditions to live long and productive lives.

In step with that, life insurance companies will even offer preferred rates to people with health issues such as anxiety, asthma, depression, high cholesterol, hypertension, weight problems, sleep apnea and others.

I don’t need life insurance while young and single

Buying life insurance when you’re young and healthy can land you a better rate, but do you really need life insurance so soon? Even if you’re healthy, and childless, life insurance may still be a good idea. Accidents can happen any time; if they do, you’ll want to leave your family enough money to pay for a funeral and wrap up your affairs. If you have debt that’s cosigned by another person, such as student loans, life insurance is especially important.

Stay-at-home parents don’t need life insurance

There’s no question that life insurance is critical for your family’s breadwinner, especially if you have kids at home. However, even stay-at-home parents should be protected by a life insurance policy. The loss of a stay-at-home parent can be a huge hit to a family’s finances; not only must the surviving parent pay medical and funeral expenses, they also have to pay for childcare now that their spouse is gone. Life insurance covers these expenses so your family doesn’t suffer.

You need 10 times your income in life insurance coverage

10 times your yearly income is a commonly cited rule of thumb when it comes to buying life insurance. But rather than relying on simplistic guidelines, you can accurately estimate your life insurance needs by using a detailed online needs calculator to determine the amount you should get. It will take into account such things as lost income, debt obligations, the cost of college education, and funeral costs to determine how much money your family needs going forward.

While life insurance can seem like an unnecessary expense when you’re just trying to keep up with the monthly bills, buying life insurance is one of the best things you can do for your family’s financial security – just like you do when insuring your car, your home, and your health.

When you’re protected by life insurance, you can rest assured that your family will be cared for no matter what happens.

About the author, Nicole Rubin

I worked in the health insurance industry for years. Every day I fielded questions from people concerning their coverage and medical bills. I learned a lot about how the industry works, the limitations and challenges health insurance companies face, and the limitations and challenges faced by their customers.

Though a lot has changed since I worked in health insurance, I’m still very interested in the industry and the ongoing debate over how medical coverage should be handled in the U.S. I created Insureabilities to provide up-to-date information on the state of health insurance in the U.S.

As parents, one of the most important lessons to pass along to your children (other than saying please and thank you and to always eat your vegetables) is how to stay out of debt and plan for the future.

This doesn’t require mastery of financial instruments – like currency futures and exotic derivatives. But knowing how to make a budget and stick to it, or how to choose the best IRAs and other retirement plans are essential to their future well-being and development.

Setting the Right Example

Unfortunately, children often learn the wrong lessons from the examples their parents set. For instance, how many four-letter words have your kids picked up from hearing you accidentally stepping on their Legos in the middle of the night on the way to the bathroom!

Bad fiscal habits are also surprisingly inheritable. In short, if you’re bad with money, it is more likely that your kids will be, too. If you’re in debt by the end of your life, it could become hereditary debt. If you leave debt to your children, it will be far more difficult for them to achieve a debt-free life, themselves.

3 Financial Identity Types

According to the decade-long Life Success research project, children fall into three categories when it comes to learned fiscal habits.

Followers: follow their parents’ example

Pathfinders: are interested in financial topics and find their own way

Drifters: don’t follow their parent’s example, but also don’t have any other strategy.

Parental Influence

Even though each child tends toward their own way of processing things, the researchers discovered that each identity style was strongly associated with a different level of parental guidance.

Children who had received some financial education, primarily modeled after their parents own financial habits identified as followers.

Children whose parents talked to them openly and frequently about finances and involved them in financial decisions identified as pathfinders.

Children who lacked these experiences identified as drifters.

Preventing Hereditary Debt with Life Insurance

One of the most important financial habits to pass on for preventing hereditary debt is to discuss and purchase term life insurance with your children. They learn that you can still be financially responsible to those who depend on you even after you die. Making sure your loved ones are cared for, the mortgage is paid off, and college expenses are covered ensures that heirs don’t inherit debt and thus breaks the chain of hereditary debt.

John Hancock announces John Hancock Aspirewith Vitality, a new, first of its kind term life insurance designed specifically for Americans living with diabetes, in collaboration with Verily, an Alphabet company, and digital healthcare company Onduo.

All John Hancock Aspire customers will also have access to an enhanced version of John Hancock Vitality along with potential to save up to 25% on their premiums.

John Hancock Aspire offers customers living with diabetes life insurance paired with an online program that provides coaching, clinical support, education, and rewards to help manage their health.

Onduo Technology: Qualifying John Hancock Aspire customers with type 2 diabetes will be eligible to access Onduo’s virtual clinic and receive a blood glucose monitoring device. When used in conjunction with the Onduo app, it provides insights into the user’s diabetes management. Onduo’s virtual care team, made up of diabetes professionals, offers personalized guidance and support regarding diet, activity, lifestyle habits and medication management. Onduo users can earn points to further boost their overall Vitality rewards and lower their premiums.

“The life insurance industry hasn’t traditionally served people living with diabetes well. When we help customers manage their diabetes by providing virtual care, education, support, incentives and rewards, we’re not only creating value for them, but also for our industry and society as a whole. That’s why we’re thrilled to work with innovative industry leaders, Verily and Onduo, to offer access to people living with diabetes to this first-of-its-kind offering. It’s time our industry started delivering more tailor-made solutions that truly help our customers.” – Brooks Tingle, President and CEO of John Hancock.

“This dynamic partnership with John Hancock unlocks the full potential for the Onduo platform, empowering people living with Type 2 diabetes to co-produce their own health at home and in mobile environments and rewards them for doing so. Through this initiative, Verily and John Hancock are pushing the envelope on the role life insurance can play in both providing financial security and helping people live longer, healthier lives.” – Andy Conrad, CEO, Verily.

John Hancock Aspire will be available to customers on November 18, 2019.

The actress has partnered with Life Happens to spread awareness about coverage accessibility.

Last month, Brooke Shields used a partnership with Life Happens to draw attention to life insurance value and accessibility.

Last month was life insurance awareness month and this partnership played a central role.

Shields partnered with the non-profit to help push forward the message of life insurance value and accessibility. It was a very direct message: that every family can and should buy coverage to ensure their loved ones are protected if the worst should happen. Death, on its own, is expensive. That said, if the deceased has dependents, then they are left in need if a main financial contributor is no longer able to provide.

Shields feels that being a mother is her most important role, even though she is also an actress, clothing designer, author and businesswoman. As a mother, she feels that it is her obligation to have life insurance. In fact, she purchased a policy even before she married because she knew she planned to have children and it was important to have these protections in place even before they were born.

Shields wasn’t taught about life insurance value or financial security while growing up.

Shields explained that finance and life insurance value was not a focus when she was growing up. Her mother never discussed these topics directly with her. That said, Shields did grow up with an understanding of how important it is not to have to depend on someone else to survive in life. This mindset served her well throughout her life as she made a priority of protecting herself financially and of being independent.

The actress’s business manager helped her to understand the finer financial details once she started working regularly. Through her manager, she learned how much she must earn and how much she needed to put in savings. This breakdown of financial basics made them far more accessible to her, so she was no longer intimidated by them.

“This is exactly what Life Happens is doing for people who don’t have a financial advisor or a team – they are providing tools and education to make life insurance accessible to all. And education and knowledge is always such a powerful position to be in,” said Shields. She spent September spreading the word about life insurance value and financial accessibility to help other people to gain a similar understanding so they can effectively do their own financial planning.

Do You Know The Average Cost Of A Life Insurance Policy?

According to MarketWatch, 40% of Americans do not have a life insurance policy and, for many years now, the majority of those who don’t have life insurance choose not to because they think it’s too expensive. LifeHappens.org has found that people assume that life insurance is up to 3x more expensive than it really is!

Term2Go

September is life insurance month, so here is our guide to understanding the true costs of life insurance.

Term2Go

Actual rate from QualityTermLife.com’s quoting system:

A 20-year-old man can get a $250,000, 30-year term life insurance policy for the price of 3 gallons of gas in California (about $13/month).

A 40-year-old woman could get $1 million of 20-year term life coverage for the cost of 12 Grande Starbucks lattes (about $45/month).

A 55-year-old woman could get $200,000 of 15-year term life coverage for the price of six cocktails (about $32 /month).

Term2Go

Experts quotes for finding the right life insurance policy:

When choosing a coverage amount, it’s best to start with what you want to accomplish. Think about what needs your family will have if you were to pass away unexpectedly. A 30-year-old with a newborn will have different needs than a 60-year-old who is thinking of retiring soon. Use a detailed online needs calculator to determine the amount you should get.

There are two main reasons to get a life insurance policy as soon as you have the need. First, rates are based mostly on age and increase as you get older. Second, life is unpredictable. Taking pressure of worrying about how loved ones will cover the mortgage or put food on the table without you will help you sleep better at night.

Prior to having my child, I did not think much about life insurance and simply lived each day as it came. Since the birth of my child, I have taken things a lot more seriously. I have gotten my health back into tip top shape and now I am making sure to save money and think about the future. It truly is amazing what a kid can do. They put things into perspective for you. After all, you have a tiny human depending on you for EVERYTHING. It’s a lot of pressure.

As I think more and more about life insurance and what it would mean to me, as a single parent, for my daughter, I have decided to choose a plan and purchase it. Below, I will talk about why I want the plan and how to go about getting one.

Why Life Insurance?

Think about it for a moment. What would happen to your family if you were to suddenly die today or tomorrow? Would they be able to sustain themselves financially? Would they be okay without you? Often times, the answer is no. I know that if I were to die today as I write this, my child would not be taken care of without a life insurance policy in place.

The reason I want to take out a policy on myself is so that my child is protected. My child’s future is secured and in place. My child will not be left dependent on welfare once I am gone, should the worst happen to me.

Before I do take out a policy though, I need to know how much to take out. This number should be one that would sustain my child through her years until she is old enough to take care of herself. Therefore, a $10,000 policy is not going to be enough should I die tomorrow and she is only 10 years old.

Basics on Getting Life Insurance

There is a lot to know about life insurance. It took me time to read, research, and learn about it before I was able to settle on what would work best for me in my situation. I learned that an insurance policy will help to:

Pay the rent or mortgage on my home

Setup a college fund for my child

Protect my child’s future

Pay off any debts I currently owe

Help to maintain my child’s standard of living

I found a nifty little calculator when I was determining how much life insurance I would need and it helped me determine that I needed a policy in the amount of somewhere between $300,000 and $500,000. This was a wakeup call to me and it really kicked me into gear.

I also learned that there are two kinds of life insurance you can buy: term or permanent. Term life costs less and is the right product for anyone with dependents, debt and minimal savings. It is straightforward to understand and easy to buy. Permanent life insurance, on the other hand, is expensive and complicated. Financial gurus, including Suze Orman and Clark Howard, do not recommend it for the average person.

Final Thoughts

Who knows when I may kick the bucket and I truly hope it is not for a long time, but it is not something that we can know and I want to make sure that my daughter is completely taken care of when the day does come. I visited QualityTermLife’s website where I could comparison shop from dozens of companies who offer term life insurance. I chose a quote at a cost of a little over $20 per month for a $500,000 policy that will cover me for 15 years. Long enough to see my daughter through college, and I am confident that with my current savings that this amount will be enough for my child.

If you want to take out a term life insurance policy, you should explore your options and find out what the recommended amount is for your loved ones to sustain their way of life. You may be surprised at how much you need, yet how affordable it is. Knowing that they will be taken care of will allow you to close your eyes each night.

Dave Chen is the main contributor and owner of Millennial Personal Finance. He puts his extra time into his blog while handling life’s responsibilities including his job as an engineer, his job as a single parent, and his love for skiing (okay, maybe that one is more of a hobby).

by David Chen, Guest Blogger

by David Chen, Guest Blogger