Term Life Insurance Quote of the Day

America's favorite term life insurance agency. Save when you compare quotes online

It’s true. This short, cute video sums it all up very nicely.

One of the most important tips comes at the very end, though. So let me call it out here: Comparison shop!

This so important because over the course of a typical 20 year term policy, saving even a few dollars per month can really add up!

QualityTermLife offers term life insurance quotes from dozens of top insurance companies, ensuring that you will get the best price.

Originally posted on Vimeo.

The infographic visualizes the fact that although 70% Americans do not have life insurance, 93% of them believe it is important to have it.

Why? At the very least, life insurance can help offset the costs of a funeral, which nowadays averages $20,000. Most importantly, it can replace the income of the primary breadwinner. It is recommended that coverage be somewhere in the neighborhood of 10 to 20 times gross income to provide financial security.

The cost of life insurance depends on the coverage amount, and the age and health of the insured. Life events like marriage, starting a family, or buying a home are all typical reasons that prompt people to buy a life insurance policy.

Life Insurance is a tiny investment to protect yourself and your loved ones in case of an emergency. Right now, rates are the lowest they have been in decades. If you don’t have this important investment in protecting the future of your home and family. Look into getting it, today. QualityTermLife let’s you compare term life insurance quotes online from dozens of the top insurers.

Source: Fidelity Life Insurance

What is the best type? How much should you purchase? Life insurance as a feature of a solid financial plan is a critical because it reduces risk, like the possibility that your family won’t have enough money if something were to happen to the income earner or care-giver.

Well, if you don’t have dependents, you probably don’t need life insurance. But, if you own a home, have children or others who depend on you, have a taxable estate or wish to leave money to charity, then life insurance can serve to protect your loved ones and the legacy you care about.

There are other types, but term life is what most people need. Important factors to consider are the length of the insurance (the term), the face amount (the amount your beneficiaries receive if you die) and the premium (how much the policy costs). Term is the most straight-foward form of life insurance (i.e. no investment features). And it is by far the most inexpensive. The way it works is that you pay the monthly or annual premium and, if the insured person dies during the term (time of coverage), the insurance company pays the beneficiary the face amount of the policy.

Beyond the need for a death benefit, there is whole life insurance. Unlike term life, it pays whether you die sooner or later. Instead of covering you for a temporary period (10, 20, or 30 years), so that you can take care of a mortgage or raising children, permanent insurance guarantees to pay a benefit whenever you die – even if you live past 100.

One common reason for owning whole life insurance is owning a taxable estate that can result in a considerable estate tax. In that case, death also provides the payout life insurance to cover the expense. You may also wish to bequeath money to a charity, which you can name as the beneficiary on the policy.

The types of things you should consider, include:

Shop with and purchase only from an independent broker – like Quality Term Life. An independent broker can show you competitive quotes from dozens of insurers. Whereas a captive agent can only sell insurance offered by one company,

As a side note, many people seem to think they can’t get life insurance because of a pre-existing medical condition or disease. But in almost all cases, there are affordable options available. Quality Term Life advisors can help you find the best insurance for your situation. Just give them a call.

If you don’t have life insurance now, be sure to add it to your overall financial plan. It is a critical risk management asset. But more importantly, it protects your loved ones’ future, giving you peace of mind – which is priceless.

Short answer: No. The reality is that the overwhelming majority of children don’t need life insurance.

While the advertisements for insuring children may appeal to your emotions, the financial fact is that a loss of a child will will actually remove a major commitment. That may sound harsh, but life insurance is for helping with the financial repurcussions of a death, and it simply costs much less not having a child than having one.

Is children’s life insurance cheap? Sure, but that is because it is rare for children to die. The sales agent will give you a great pitch about how low the cost is, but if you figure the return on investing all those years of premiums into a Roth IRA, or 529 college account, you’ll see that it’s really not such a great deal at all. There are far better investment vehicles that will help you and your child.

The main reason for life insurance is to provide financial security to the family in the event that an income earner dies. So, unless your child is a child movie or rock star, there is probably no reason for you to buy children’s insurance.

On the other hand, far too many parents who are considering children’s insurance are underinsured themselves or simply aren’t insured at all. Your children are much more at risk of losing you, than you are of losing them.

Visit an online insurance website with a good needs calculator. After you figure out how much insurance you should have, use the quote engine to see just how affordable an adequate amount of insurance is.

Quality Term Life’s website features an easy to use needs calculator, and you can compare rates from dozens of leading term life insurance companies to get the best price.

Live life – with confidence

Protecting the financial future of children is something concerns all parents. But in the case of a parent with a special needs child, planning for a future when you may no longer be around can extend into your child’s adulthood.

Protecting the financial future of children is something concerns all parents. But in the case of a parent with a special needs child, planning for a future when you may no longer be around can extend into your child’s adulthood.

In this case, the typical term life insurance policy – with a cover equal to 8-10 times annual income plus debt obligations – won’t be sufficient. On average, children are dependent on parents financially for up to 25 years. But special children may be financially dependent for many years beyond that – with the very real likelihood that their parents will not be around when they are still dependent.

The amount and term (years) of the life coverage a parent in this situation should have requires that this longer view be taken into consideration. Of course, how much more coverage you need and for how much longer depends on your individual financial circumstances and on how independent your child is likely to be.

Fortunately, today, many special children can live quite independently, some even financially so. As a parent, you work hard to give your special someone as much freedom as possible. With the right life insurance, you can help to continue it long after you are gone.

For help on the details, use our needs calculator and quote engine, and then contact one of our insurance experts consult a Quality Term Life insurance expert who will help you find the most affordable policy.

Live life – with confidence

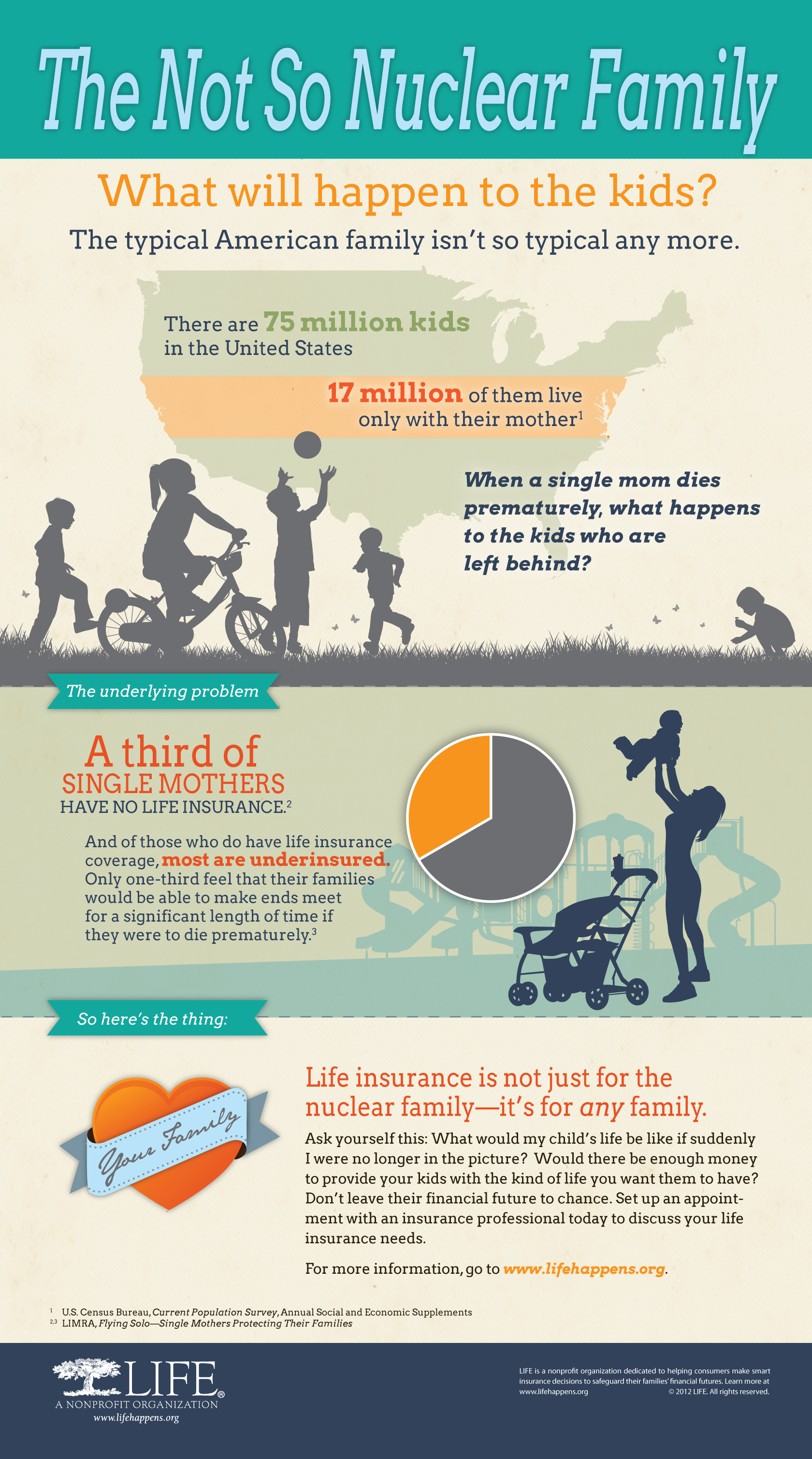

An info graphic from LifeHappens.org summing up a recent survey on single Moms and life insurance. The basic principal applies just as well to single Dads, too!

We understand that finances can be squeezed when you’re a single parent. With rates at an all time low, life insurance can be surprisingly affordable.

It may come as no surprise that the reasons why people buy life insurance depends greatly on their age – the time of life they are in.

Northwestern Mutual conducted a survey that sought to discover the different reasons why people buy life insurance according to age and lifestyle.

Over 55:

The poll found that 36% of Americans over 55 who own life insurance bought it as a direct result of getting married while 31% bought it to utilize as part of a retirement plan.

Those 55 and up derive the most peace of mind knowing that they will have enough money to live in retirement.

Forty-five to 54 year olds who own life insurance were spurred to do so because of marriage (39%) followed by retirement planning (25%) and home ownership (25%). This age group felt most comfortable due to their purchase of life insurance with 69% of them saying that they feel secure as a result of owning life insurance.

34% of those between 35 and 44 and 36% of those between 45 and 54 derive the most peace of mind knowing that their family will be provided for in case of an unexpected death while 68% of those between 18 and 34 and 58% of those between 45 and 54 who have insurance were likely to have purchased it to provide for their loved ones.

Americans who are between 18 and 34 years old who have some degree of life insurance protection are most likely to have been prompted to purchase it because of the birth of a child. When this group was asked what gave them the greatest peace of mind, 35% of 18 to 34 year olds felt that it was knowing that their debts were paid off.

“It is important to have a financial plan that can both support you and evolve across the span of your lifetime as your financial situation changes. Life insurance can be a stable and yet flexible cornerstone of a financial plan—protection if you need it while also helping you to meet financial goals at various life stages,” said David Simbro, senior vice president at Northwestern Mutual.